How to Finance a Tractor

Costs, credit requirements, new vs used, and approval process for tractor financing. Step-by-step guide for farmers.

Read moreConnect with lenders who understand agriculture. Equipment financing for tractors, combines, and farm equipment. SBA loans for land and barns. Working capital for seed, fuel, and inputs during the growing season. One application, we match you with the right programs.

Agricultural businesses operate differently from most other industries. Revenue is seasonal—you incur costs for seed, fertilizer, fuel, and labor during planting and growing, then get paid at harvest or when livestock sells. The lag between spring planting and fall harvest—or between calving and sale—creates cash flow gaps that can stall operations and limit growth. Standard bank loans often don't align with how farmers actually run their businesses.

That's why agriculture-specific financing matters. Lenders who understand the industry evaluate your crop history, acreage, and seasonal cycles—not just static financials. They structure equipment loans around the useful life of tractors and combines, working capital around planting and harvest, and SBA loans for land and barns when you're ready to expand. Axiant Partners connects row-crop farmers, livestock operations, and specialty growers with lenders who get agriculture. One application, we match you with programs suited to your business profile. See all industries we serve. Apply now to see what you qualify for.

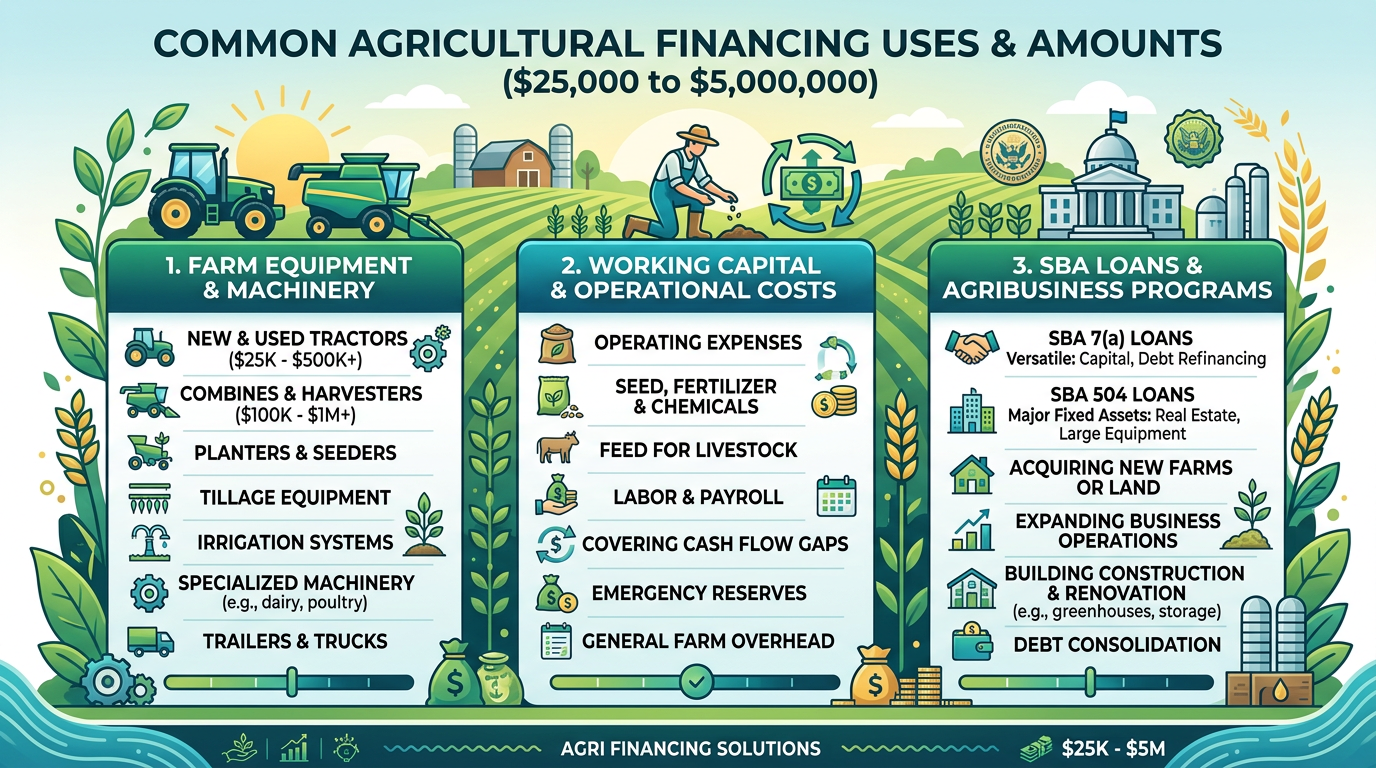

Farmers and ranchers need capital for tractors, combines, inputs, land, and growth. From seasonal operating needs to long-term equipment and land purchases, here are the most common uses—and how we connect you with the right product.

Tractors, combines, sprayers, hay balers, skid steers, and grain handling. Equipment financing spreads the cost over the asset's useful life instead of tying up cash. Many lenders specialize in ag equipment and understand resale value, hours, and seasonal usage. Typical terms 36-84 months. Browse equipment by type.

Seed, fertilizer, fuel, and labor during the growing season when harvest income is months away. Working capital loans bridge the gap between planting and harvest—or between calving and sale. Terms can align with your seasonal cycle. Essential when expanding acreage or managing input costs. Explore farm working capital.

SBA 7(a) and 504 loans for land acquisition, barns, grain storage, equipment, and working capital. Lower down payments (10% for 504 real estate), longer terms (10-25 years), competitive rates. Use 7(a) for flexibility; 504 for owner-occupied land and buildings. Plan for 30-60+ days. View SBA loans for agriculture.

Revolving credit for inputs, repairs, and off-season needs. Draw when planting or preparing; repay when harvest or livestock sales arrive. Ideal for seasonal cash flow where needs fluctuate. Many farmers use a line alongside equipment and SBA financing. Explore farm line of credit.

Purchase or refinance land, barns, grain storage, and agricultural property. SBA 504 and agricultural mortgages build equity while freeing capital for equipment and inputs. Owner-occupied property often qualifies for favorable terms. Stop leasing; build equity instead. Explore farm & land financing.

Buy another farm, acquire acreage, or purchase an existing operation. SBA 7(a) loans finance acquisitions—often with as little as 10% down. Seller financing and thorough documentation improve approval odds. Grow through acquisition when organic growth isn't enough. SBA acquisition financing.

Agriculture financing sizes vary by product, use of funds, and business profile. Here are representative ranges we see across the U.S.:

Your actual amount depends on revenue, credit, collateral, acreage, and lender. Use our financing calculator to estimate monthly payments. Apply now to get matched with programs for your situation.

Agriculture-specific financing offers advantages that generic business loans often cannot match. Here's why farmers nationwide turn to specialized lenders:

Equipment financing often receives decisions in 24-48 hours. When you need a tractor for planting or a combine for harvest, you can't wait 60 days. Working capital and lines of credit can fund in days to a few weeks. SBA takes longer but offers terms others can't match.

Spread equipment costs over 36-84 months instead of one lump sum. Keep cash for seed, fuel, and unexpected repairs. Working capital loans bridge seasonal gaps without depleting reserves. Match financing structure to your cash flow—not the other way around.

Agriculture lenders evaluate crop history, acreage, seasonal cycles, and industry experience—not just financials. They structure loans around equipment useful life and harvest schedules. Terms that fit how you actually operate.

Equipment today, working capital for planting, SBA land when you're ready to expand. Many farmers use a mix. We connect you with lenders who offer the full suite—so you're not juggling five different banks for five different needs.

We connect you with lenders who offer equipment financing, SBA loans, working capital, and lines of credit. Understanding the options helps you choose the right fit—and we guide you through that decision.

Axiant Partners connects you with agriculture lenders and guides you from application to funding.

Tell us about your operation, equipment needs, acreage, and use of funds. One application goes to multiple agriculture lender partners. We determine whether equipment, working capital, SBA, or a combination fits best.

Our team analyzes your profile and identifies lenders whose programs align with your needs. Equipment-only? Working capital for planting? SBA for land? We connect you with the right programs.

Equipment financing often requires minimal docs—application, bank statements, equipment quote. SBA and larger working capital need more. We tell you exactly what's needed and keep the process moving. Equipment decisions in 24-48 hours; SBA 30-60+ days.

Once approved, funds disburse per your loan type. Equipment financing—lender pays vendor or you. Working capital—deposited to your account. SBA—per closing docs. You're funded and ready to plant, harvest, or expand.

Equipment financing: 24-48 hours. Working capital: days to weeks. SBA: 30-60+ days. Apply now to get started.

Farmers and ranchers frequently finance tractors, combines, and specialized equipment. Below are common types, typical cost ranges, and why businesses finance them. Lenders who specialize in agriculture equipment understand depreciation, resale value, and seasonal usage—often resulting in better terms and faster decisions.

Tractors power planting, tillage, haying, and material handling. New row-crop and utility tractors typically cost $80,000–$400,000 or more depending on horsepower and features. Many farmers finance tractors to add capacity or replace aging units without large upfront outlays.

How to finance a tractor

Combines harvest grain, corn, soybeans, and other row crops. New combines typically cost $300,000–$500,000 or more. Financing helps farmers add or replace harvest capacity and match payments to seasonal revenue.

How to finance a combine

Skid steers handle feeding, material handling, and cleanup on livestock and crop operations. They typically cost $25,000–$75,000. Financing helps farmers add versatile equipment for daily tasks.

How to finance a skid steer

Hay balers produce round or square bales for livestock feed and sale. Balers typically cost $20,000–$80,000 or more. Financing helps livestock and hay producers add or upgrade baling capacity.

How to finance a hay baler

Sprayers apply fertilizer, herbicides, and pesticides to crops. Self-propelled and pull-type sprayers range from roughly $30,000 to $400,000 or more. Financing helps farmers improve application efficiency and crop protection.

How to finance a sprayer

Grain augers, conveyors, and bins move and store harvested grain. Equipment costs range from roughly $10,000 to $100,000 or more depending on capacity. Financing helps farmers add storage and handling to improve marketing flexibility.

How to finance grain equipmentWhen you need a tractor for planting, a combine for harvest, or a sprayer for the growing season, you can't wait months. Agriculture equipment financing delivers decisions in 24-48 hours for many applications. Lenders who specialize in farm equipment understand your industry—they evaluate the asset, your crop history, and acreage. New or used, single unit or fleet, equipment financing preserves cash and matches payments to the equipment's productive life. Whether you're a row-crop farmer, livestock operator, or specialty grower, we connect you with lenders who finance the equipment you need. See our full equipment financing overview or apply now to get matched.

Agriculture revenue is seasonal—you pay for seed, fertilizer, and fuel during planting and growing, then get paid at harvest or when livestock sells. Working capital loans bridge that gap. Cover planting inputs, fuel for fieldwork, labor during busy seasons. Terms can align with your harvest schedule, so you're not stuck with a 12-month loan when income arrives once or twice a year. Farmers use working capital to expand acreage, manage input costs, and smooth cash flow between seasons. If you're tired of juggling payables while waiting on harvest, working capital financing can change the equation. Explore farm working capital or apply to see your options.

Requirements vary by product and lender. Here's what most agriculture lenders consider:

Strong operations with clear use of funds and solid documentation typically qualify for favorable terms. Challenged credit? Options exist—terms may differ. Apply now and we'll match you with lenders whose criteria fit your profile.

We focus on connecting farmers with the right lenders and moving your application forward efficiently.

One application, multiple options, support at each stage. Apply now to get started.

Farmers can access equipment financing for tractors, combines, and farm equipment; SBA 7(a) and 504 loans for land, barns, and grain storage; working capital loans for seed, fertilizer, fuel, and labor; and lines of credit for seasonal inputs. Amounts typically range from $25,000 to $5,000,000 depending on use and business profile. Apply to see what you qualify for.

Equipment financing often receives decisions within 24-48 hours. SBA loans typically take 30-60+ days. Working capital and lines of credit can fund in days to a few weeks depending on lender and documentation. Need a tractor for planting? Equipment financing is usually the answer.

Yes. Many lenders finance both new and used tractors, combines, and farm equipment. Used equipment may have shorter terms (36-60 months) and rates based on age, hours, and condition. Resale value and useful life affect terms. See our guide to used equipment financing.

Equipment financing programs often accept 550+ FICO. SBA loans typically favor 650-680+ credit. Working capital and lines of credit vary by lender. Strong credit improves terms; options exist for challenged credit with different structures. Apply and we'll match you with lenders that fit your profile.

Farmers use working capital to cover seed, fertilizer, fuel, and labor during the growing season when harvest income is months away. Terms can align with seasonal cycles—plant in spring, repay after harvest. Essential for planting and managing input costs.

Yes. SBA 7(a) and 504 loans finance tractors, combines, and farm equipment. 7(a) is flexible for general equipment; 504 suits long-lived machinery. Approval typically 30-60 days. If you need equipment faster, equipment-only financing often funds in 24-48 hours. Compare SBA vs equipment financing.

Explore our most popular articles on agriculture and equipment financing. For equipment-specific guides by type, see Equipment by Type. For all articles, see Equipment Financing Articles.

Costs, credit requirements, new vs used, and approval process for tractor financing. Step-by-step guide for farmers.

Read moreCredit requirements for equipment loans and leases. Programs for 550+, 600+, 700+ FICO. Improve approval odds.

Read moreYes. Guide to used equipment financing—terms, rates, age limits, and what lenders evaluate for pre-owned tractors and combines.

Read moreCosts, terms, and approval process for combine financing. Essential for row-crop harvest capacity.

Read moreWe also provide financing for forestry and landscaping (nurseries) businesses. View all industries.

Farmers and ranchers need financing that fits seasonal cycles and cash flow. Axiant Partners connects agricultural businesses with lenders that offer equipment loans, working capital, SBA loans, and more. Submit your information once and we match you with programs suited to your business profile.