Business Line of Credit vs Term Loan: Which Is Better?

Compare flexibility, cost, and when each structure fits your capital needs.

Read moreRevolving credit from $10,000 to $2,000,000+. Draw as needed, pay interest only on what you use. Decisions often in 24-48 hours. Ideal for payroll, inventory, seasonal gaps, and growth.

Cash flow doesn't always align with opportunity—especially for small businesses. Revenue fluctuates. Customers pay in 30, 60, or 90 days. Seasonal spikes demand upfront investment. Growth requires capital before revenue arrives. For most businesses, a traditional term loan locks you into fixed monthly payments on a lump sum—whether you need it all at once or not.

A business line of credit solves this by giving you a pre-approved credit limit you can draw from as needed. Use $20,000 this month for payroll, repay it when invoices clear, then draw again for inventory next quarter. You pay interest only on what you actually use—unlike a term loan where you pay on the full amount from day one. It works like a business credit card with much higher limits and often lower rates.

Axiant Partners connects established businesses in all 50 states with lenders offering both unsecured and secured lines. Whether you need a $50,000 safety net or a $500,000 working capital facility, we match you with programs that fit your revenue, credit profile, and goals. Compare with working capital loans if you need a lump-sum solution. Apply today and get a decision quickly—many lenders respond within 24-48 hours.

Lines of credit are built for flexible working capital. From payroll and inventory to receivables gaps and growth initiatives—here are the most common ways U.S. businesses use them:

Cover payroll during slow periods or when receivables are delayed. Keep your team paid and operations running without draining reserves. A line of credit bridges the gap between when you need to pay and when cash arrives.

Stock up before busy seasons, buy in bulk for better pricing, or bridge the gap between ordering and selling. Retail, hospitality, and distribution businesses rely on lines to fund inventory without tying up all available cash.

When customers pay in 30-90 days but you need to pay vendors now, a line bridges the timing gap. Construction, professional services, and B2B companies use revolving credit to keep projects moving while waiting on payments.

Fund new locations, marketing pushes, hiring, or short-term projects. Draw what you need when you need it—no need to over-borrow or pay interest on idle capital. Use the line to seize opportunities as they arise.

Consolidate high-cost merchant cash advances, factor receivables, or replace expensive short-term financing with lower-cost revolving credit. Many businesses use a line to improve cash flow and reduce overall cost of capital.

Have a safety net for unexpected repairs, opportunities, or market changes. When equipment breaks, a key client pays late, or a deal requires quick action—access capital within 24-48 hours without scrambling for alternatives.

Credit limits depend on revenue, credit strength, time in business, and whether the line is secured or unsecured. Here are representative ranges we see across the U.S.:

Your actual limit depends on revenue, credit, time in business, and lender. Use our financing calculator to estimate costs. We match you with lenders whose programs align with your profile.

A line of credit offers advantages that term loans and credit cards often can't match. Here's why companies nationwide apply for revolving credit:

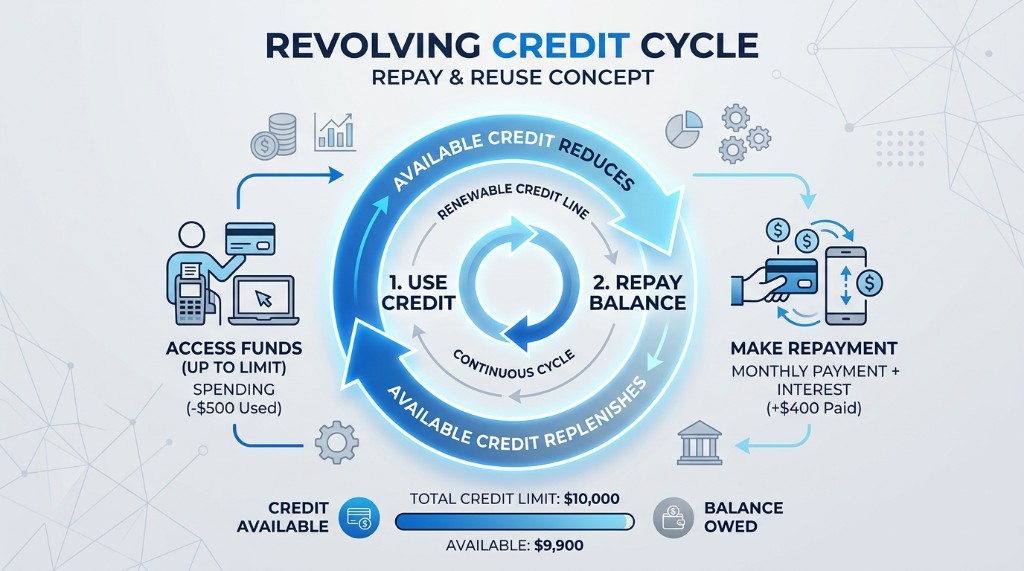

Interest accrues only on the amount you draw. Leave the rest undrawn and pay nothing on it—unlike a term loan where you pay on the full amount from day one. Access to capital without the cost until you need it.

Repay and reuse. As you pay down the balance, that credit becomes available again. Use it as often as you need during the draw period—seasonal cycles, project-by-project, or as an ongoing reserve.

No restrictions on how you use the funds—payroll, inventory, rent, marketing, refinancing, or opportunities. Use it for what your business needs, when it needs it. No lender approval for each use.

Once approved, draws typically fund within 24-48 hours. When cash flow tightens or an opportunity appears, you can act quickly. No lengthy application process for each draw—the facility is already in place.

We connect you with lenders who offer several line of credit structures. The right fit depends on your assets, credit, revenue, and whether you prefer unsecured or secured financing.

No specific collateral required. Approval is based on revenue, credit strength, and time in business. Fewer restrictions and faster to set up—no UCC filings or asset appraisals. Rates are typically higher than secured lines, but you gain speed and simplicity. Ideal for businesses with strong revenues and consistent cash flow who want flexible access without pledging assets.

Backed by receivables, inventory, or other business assets. May require a UCC filing and periodic reporting. Lower rates and higher limits—lenders take less risk when collateral supports the facility. Ideal for asset-heavy companies with significant receivables or inventory who want to maximize credit capacity and minimize cost.

When time matters, some lenders offer faster decisions—often within 24-48 hours—for lines typically up to $50,000-$150,000. Streamlined documentation and minimal back-and-forth. Suited for urgent needs like payroll gaps or inventory deadlines. Eligibility and amounts vary by lender and profile.

For established companies (typically 2+ years) with consistent revenue, lenders may offer lines from $50,000 to $500,000. Decisions usually in 3-5 business days. Designed for businesses that need ongoing working capital. Actual limits depend on revenue, credit, and time in business.

Asset-backed lines—often $250,000 to $2,000,000+—use receivables, inventory, or other collateral. Lower rates and higher limits when strong collateral supports the facility. Requires UCC filing and asset verification. Built for asset-heavy companies with significant revenue.

Options for companies with 1-2 years in business are more limited; most programs prefer 2+ years. Some lenders consider newer businesses with strong credit (often 680+) and solid revenue, with limits typically $10,000-$75,000. Apply to see what may be available for your profile.

Some lenders work with businesses in the 550+ FICO range. Rates and limits typically reflect higher risk—expect higher rates and lower limits than prime offers. Qualification depends on revenue, time in business, and overall profile. We can help match you with programs that may fit.

Requirements vary by lender and program, but many businesses may qualify if they have:

We work with multiple lenders—if one program doesn't fit, another might. The only way to know what you qualify for is to apply. Start your application today.

Axiant Partners connects you with lenders and guides you from application to funding.

Tell us about your business, revenue, and how much credit you need. A single application goes to multiple lender partners. We gather the basics—no lengthy forms up front.

We'll request bank statements, tax returns, and basic business info—only what lenders need to evaluate your application. We keep it streamlined so you can get to a decision quickly.

We match your profile to suitable lenders and present offers. Decisions often arrive within 24-48 hours for expedited programs; 3-5 days for larger facilities. Compare terms and select the option that fits best.

Once approved, the facility is in place. Draw funds as needed—typically available within 24-48 hours of each draw request. Use it for payroll, inventory, growth, or reserves. Repay and reuse as your business demands.

Many lenders respond within 24-48 hours.

Retail, hospitality, and seasonal businesses face predictable cash flow swings. Revenue spikes during holidays or peak seasons—but you need capital upfront to stock inventory, hire staff, and market. A line of credit lets you prepare for the rush without draining reserves during slow months. Draw when you need it, repay when cash flows in. Typical limits range from $25,000 for smaller operations to $500,000+ for established retailers.

Contractors and service businesses often need to fund payroll and materials before invoices are paid. Projects start with upfront costs—labor, supplies, equipment—while payment may come 30, 60, or 90 days later. A revolving line bridges the gap between project start and payment. Cover labor, buy supplies, and keep jobs moving. Use it project-by-project or as an ongoing reserve. Construction and service businesses commonly use lines from $50,000 to $250,000+.

We work with businesses across many industries, including:

Our goal is to provide financing solutions that support business growth—regardless of industry.

Explore related financing: Working Capital Loans (term loans for ops) · Business Term Loans (lump-sum) · Equipment Financing (asset-specific) · All services

We focus on connecting you with the right lender and moving your application forward efficiently.

One application, multiple options, and support at each stage. Our goal is to help you secure the financing your business needs to grow. Apply today.

Once approved and the facility is in place, funds are typically available within 24-48 hours of a draw request, depending on the lender. The initial approval process may take 24-48 hours for expedited programs or 3-5 business days for larger facilities. Once the line is open, each draw funds quickly.

Credit limits typically range from $10,000 to $2,000,000+, depending on revenue, credit, time in business, and structure (secured vs. unsecured). Established businesses with strong revenue often qualify for $100,000 to $500,000+ unsecured; secured lines can reach $1-2M+ with receivables or inventory as collateral. We connect you with lenders whose programs align with your profile.

Unsecured lines require no specific collateral; approval is based on revenue and credit. Secured lines use business assets (receivables, inventory, equipment) and may offer lower rates and higher limits. The right choice depends on your assets and goals. See do you need collateral for a business line of credit for more detail.

Most programs require 2+ years in business. Startups (under 2 years) may find alternatives such as term loans or equipment financing designed for newer businesses. Some lenders offer lines to companies with 1+ years and strong credit—apply to see your options.

Requirements vary by program. Many programs accept 550+ FICO. Strong credit (680+) typically unlocks better rates, higher limits, and unsecured options. Lenders exist for challenged credit—terms may reflect risk, but you can still access revolving capital. See credit score requirements for more detail.

Explore our most popular articles on business lines of credit.

Compare flexibility, cost, and when each structure fits your capital needs.

Read moreCompare SBA loans vs lines of credit: terms, flexibility, approval timelines, and when to use both.

Read moreSee approval tiers, underwriting factors, and how to improve your odds.

Read moreTypical approval timelines and how to speed up your application.

Read moreIf your business needs flexible revolving credit, our team can help you explore available options. Submit an application today—we'll match you with lenders and guide you through the process. Many decisions arrive within 24-48 hours.