How Much Can You Qualify for with a Business Term Loan?

Revenue, DSCR, credit, and structure determine approval amounts. Typical range $10,000 to $5,000,000+.

Read moreBusiness term loans for U.S. companies—$10,000 to $5,000,000+. One application, multiple lenders. Expansion, acquisition, equipment, refinancing. Predictable payments. Apply today and secure the capital your business needs.

When your business needs a defined amount of capital for a specific project—expansion into new markets, acquiring another company, purchasing equipment, refinancing existing debt, or funding a renovation—a business term loan delivers the lump sum you need with predictable monthly payments. Unlike a line of credit where you draw and repay as needed, a term loan gives you the full amount upfront and a clear repayment schedule. You know exactly what you're borrowing, what you'll pay each month, and when you'll be done.

That predictability matters for budgeting and planning. Whether you're opening a second location, buying out a partner, upgrading your facility, or consolidating high-cost debt, a term loan lets you lock in your capital and focus on execution. Axiant Partners connects businesses in all 50 states with lenders who offer term loans from $10,000 to $5,000,000+—often with decisions in 3-10 business days for mid-sized deals. We match your profile to the right structure: secured or unsecured, short-term or long-term, based on your revenue, credit, and use of funds.

One application goes to multiple lender partners. We walk you through documentation, compare offers, and help you close. Apply now to see what you qualify for.

Business term loans are built for one-time capital needs where you know the amount and the purpose. Here's how businesses use this financing:

Open a new location, enter a new region, or scale into adjacent services. Expansion requires upfront capital—real estate buildout, inventory, marketing, hiring. A term loan funds the full initiative so you can execute without piecemeal financing.

Mergers and acquisitions demand significant capital. Whether you're buying a competitor, a supplier, or a complementary business, a term loan can fund the purchase price and integration costs with structured repayment that aligns with the deal.

When you prefer to own equipment outright or need capital for a large purchase, a term loan provides the lump sum. Compare equipment financing for lease options; term loans suit businesses that want ownership from day one.

Consolidate high-rate merchant cash advances, credit lines, or other business debt into a single term loan with lower rates and predictable payments. Refinancing can improve cash flow and simplify your balance sheet.

Upgrade your facility, relocate to a larger space, or invest in buildout. Construction and renovation costs are typically one-time and substantial—a term loan spreads the expense over monthly payments while you improve your operations.

Major marketing campaigns, product launches, or strategic initiatives often require upfront investment. A term loan funds the effort so you can execute without draining working capital or sacrificing day-to-day operations.

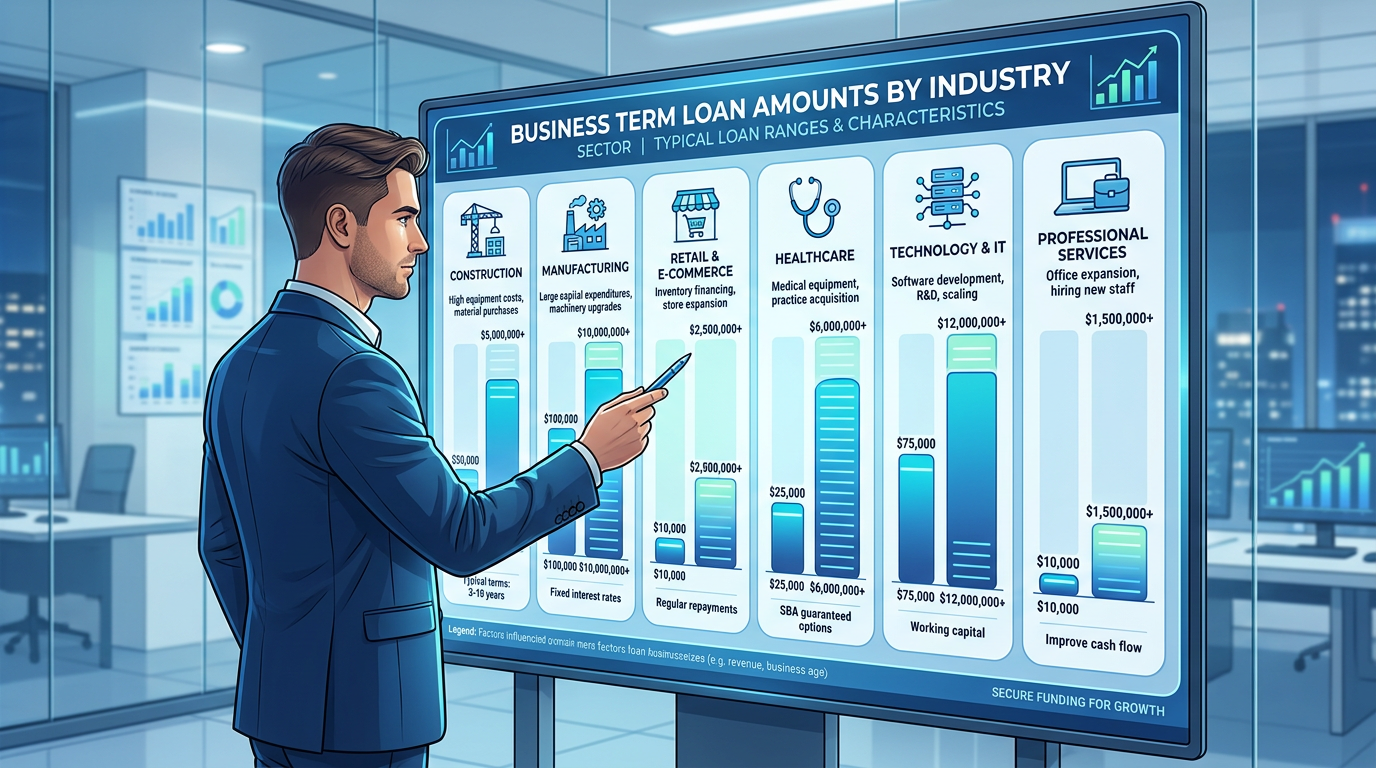

Term loan amounts vary by revenue, credit, collateral, and use of funds. Here are representative ranges we see across the U.S.:

Your actual amount depends on revenue, credit, debt service coverage, and lender. Use our financing calculator to estimate monthly payments.

Term loans offer several advantages when you need defined capital for a specific project. Here's why businesses nationwide choose them:

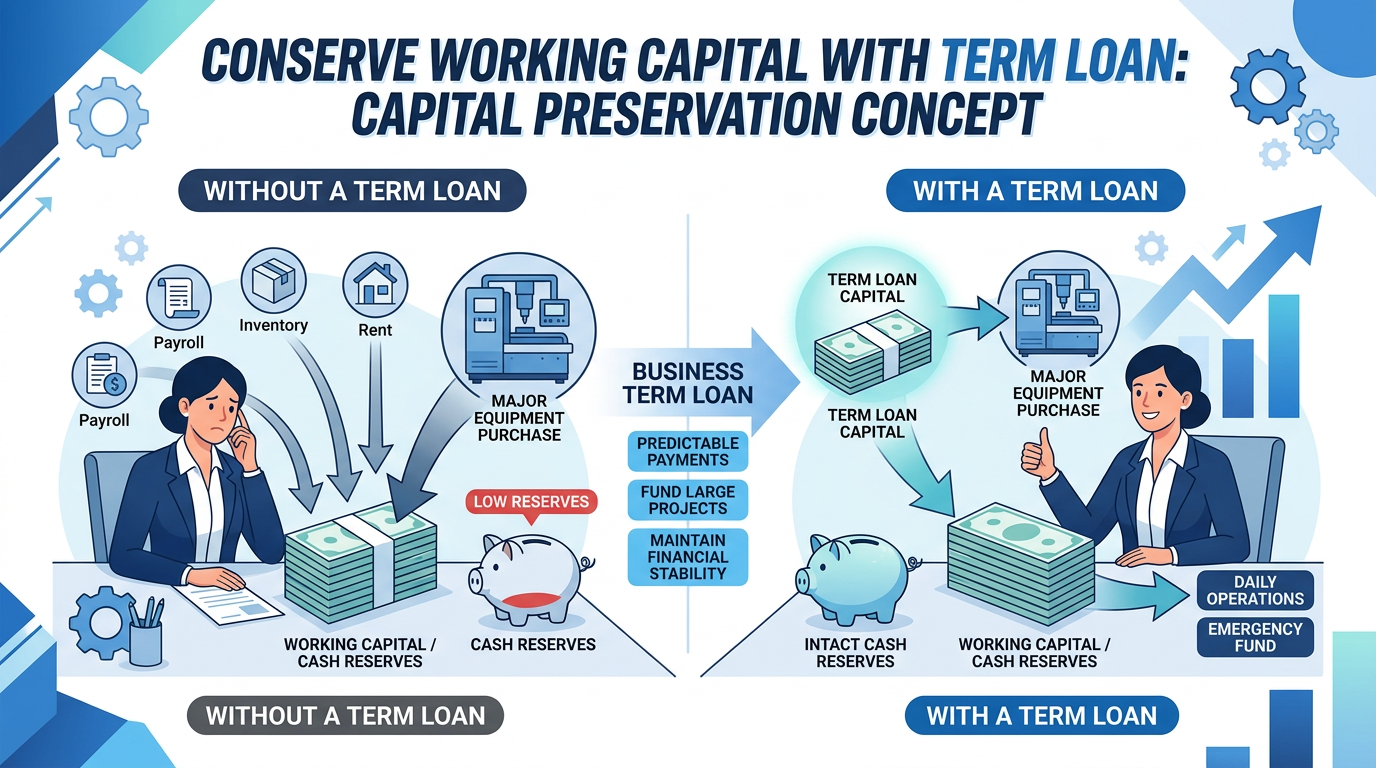

Borrow for the project instead of depleting reserves. Keep cash on hand for payroll, inventory, and opportunities. A term loan funds the initiative while you maintain operational flexibility.

Mid-sized term loans often receive decisions in 3-10 business days. Clean documentation and complete applications accelerate the process. We coordinate with lenders to keep your deal moving.

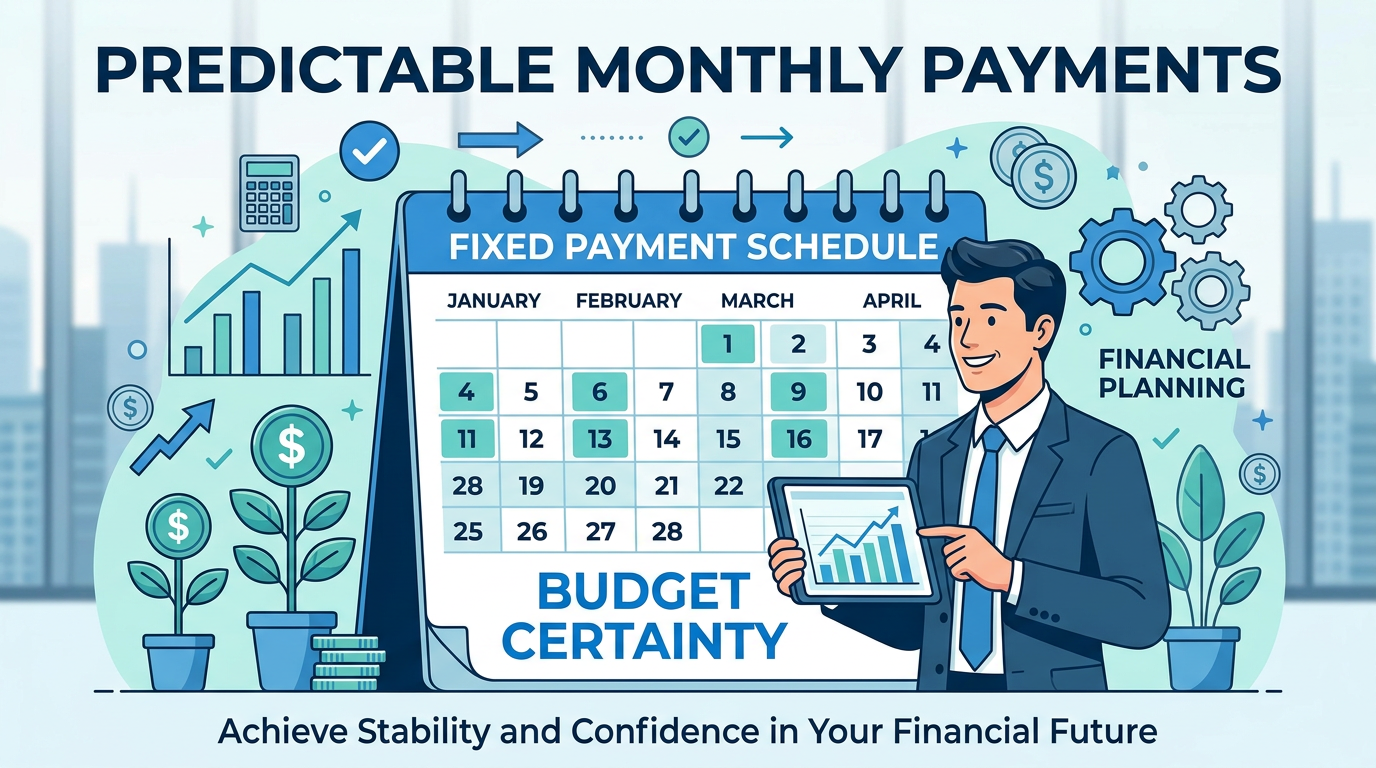

Fixed monthly payments and a set repayment schedule. No surprises—you know exactly what you owe and when. Budget with confidence and plan for the life of the loan.

Secured or unsecured, short-term or long-term—we match your profile to the right structure. Whether you have collateral to pledge or prefer an unsecured option, lenders exist for your situation.

We connect you with lenders who offer several term loan structures. The right choice depends on your collateral, credit, timeline, and use of funds.

Backed by business assets—equipment, real estate, inventory, or receivables. Secured loans typically offer lower rates, longer terms (up to 84 months or more), and higher amounts. Best when you have collateral to pledge and want the most competitive terms. The asset secures the loan, which can make approval easier for lenders.

No specific collateral required. Lenders rely on revenue, credit, and cash flow. Unsecured loans often have shorter terms and may carry higher rates, but they're available for qualified businesses that prefer not to pledge assets. Best for businesses with strong credit and consistent revenue.

SBA-guaranteed loans offer longer terms (up to 10+ years for real estate, 10 years for equipment, 7 years for working capital) and competitive rates. The SBA process takes longer (30-90+ days) but suits established businesses with time to complete full underwriting. See our SBA loans page for details.

When time matters. Many lenders fund up to $250,000 with decisions in 3-5 business days—streamlined applications and minimal documentation. Suited for urgent needs: acquisition deadlines, equipment purchases, or refinancing high-cost debt.

For scaling businesses. Lenders offer financing up to $500,000 with terms to 84 months. Decisions usually in 5-10 business days. Designed for established companies with consistent revenue and clear use of funds.

Deals above $500,000—acquisitions, real estate, large equipment, or recapitalization—are structured with terms to 84 months or longer. Review typically completes in 1-3 weeks. Built for significant capital needs.

Lenders exist for companies under two years in operation. SBA loans and certain alternative programs serve newer businesses. Solid personal credit, credible revenue, and a clear business plan improve odds. We connect you with options that fit your profile.

B, C, or D credit? We work with lenders who structure deals for businesses rebuilding their profile. Rates and structure may reflect risk, but qualified borrowers can still secure the capital needed to grow. Refinancing into a better structure later is often possible.

Both provide capital—but the structure is different. Choose based on your need:

| Feature | Business Term Loan | Line of Credit |

|---|---|---|

| Funding | Lump sum upfront | Revolving—draw as needed |

| Repayment | Fixed monthly payments | Pay on amount drawn; reuse |

| Best For | Defined project, one-time need | Ongoing cash flow, fluctuating needs |

If you need a specific amount for a specific purpose, a term loan is often the better fit. If your needs fluctuate—payroll gaps, seasonal inventory, receivables timing—a business line of credit may suit you. Many businesses use both.

Requirements vary by lender and program, but many businesses may qualify if they have:

Lenders evaluate debt service coverage ratio (DSCR), time in business, industry, and use of funds. Secured loans may have additional collateral requirements. Apply to see what you qualify for.

Axiant Partners connects you with lenders and walks you through the process from application to funding.

Tell us about your business, how much you need, and what you'll use the funds for. A single application goes to multiple lender partners. The more detail you provide, the better we can match you.

We'll ask for bank statements, financials, and other documentation—only what lenders require. Clean, organized records speed the process. We'll guide you through what's needed.

We match your profile to suitable lenders and present offers. Mid-sized deals often receive decisions within 3-10 business days. Compare terms, rates, and structure—then select the best fit.

After approval, complete closing documentation. Funds disburse to your account—typically within a few days to two weeks depending on deal size. You deploy capital where it's needed.

Mid-sized term loans: decisions often in 3-10 business days.

Opening a new location, entering a new market, or scaling into adjacent services requires upfront capital. Real estate buildout, inventory, marketing, and hiring—expansion is capital-intensive before revenue from the new initiative arrives. A business term loan funds the full project with a lump sum and predictable repayment, so you can execute your growth plan without draining reserves or juggling multiple financing sources.

Typical amounts range from $100,000 for smaller expansions to $1,000,000+ for multi-location rollouts. Terms often extend to 60-84 months. Apply now to see what you qualify for.

Acquiring another business—a competitor, supplier, or complementary operation—demands significant capital. Purchase price, integration costs, and working capital for the combined entity add up. A term loan can fund the acquisition with structured repayment that aligns with the deal's economics. Lenders evaluate the combined entity's cash flow, your track record, and the strategic rationale. Strong financials and a clear integration plan improve approval odds.

Typical amounts range from $200,000 for smaller acquisitions to $2,000,000+ for larger deals. Apply now to explore acquisition financing.

We work with businesses across many industries, including:

Our goal is to provide financing solutions that support business growth—regardless of industry.

Explore related financing: Working Capital Loans (ops, payroll) · Business Line of Credit (revolving) · Equipment Financing (asset-specific) · All services

We focus on connecting you with the right lender and moving your application forward efficiently.

One application, multiple options, and support at each stage. Our goal is to help you secure the term capital your business needs to grow.

A business term loan delivers a fixed lump sum upfront, repaid over a set term (typically 12-84 months) with predictable monthly payments. Best for defined capital needs: expansion, acquisition, equipment, refinancing, or renovation. Unlike a line of credit, you receive the full amount at once and repay on a fixed schedule.

Amounts typically run from $10,000 to $5,000,000+, depending on revenue, credit, collateral, and use of funds. Established businesses with strong financials often qualify for larger amounts. Use our calculator to estimate payments. Apply to see your options.

Small to mid-sized term loans often receive decisions within 3-10 business days. Larger structured facilities may take 2-6 weeks. SBA term loans typically take 30-90+ days. Clean documentation and complete applications speed the process.

Term loans provide a lump sum with fixed repayment—best for one-time needs (expansion, acquisition, equipment, refinancing). Lines of credit offer revolving access—draw, repay, reuse—best for ongoing, fluctuating needs. Many businesses use both. Compare business lines of credit.

Many programs prefer 680+ FICO for best rates. Some lenders work with 550+; terms may reflect risk. Strong revenue, time in business, and low existing debt improve approval odds. Apply to see what you qualify for.

Secured loans use business assets as collateral—often lower rates, longer terms, higher amounts. Unsecured loans require no specific collateral; lenders rely on revenue and credit. We match you with the structure that fits your profile. Secured vs unsecured term loans.

Explore our most popular articles on business term loans.

Revenue, DSCR, credit, and structure determine approval amounts. Typical range $10,000 to $5,000,000+.

Read moreTypical credit score tiers, lender preferences, and what improves approval odds.

Read moreCompare collateral, rates, approval speed, and loan amounts. Choose the right structure.

Read moreCompare structure, cost, and flexibility to choose the right financing path.

Read moreIf your business needs lump-sum capital for expansion, acquisition, equipment, refinancing, or another defined project, our team can help you explore available options. Submit an application today to get started. We'll match you with lenders and guide you through the process.