What Is a Merchant Cash Advance and How Does It Work?

Structure, factor rates, holdback repayment, and when MCA fits your business.

Read moreUpfront capital repaid as a percentage of card sales or daily bank deposits. $5,000 to $500,000. Funding often in 1-3 days. For restaurants, retail, salons, and businesses with strong card volume. One application, we match you with the right provider. Apply today.

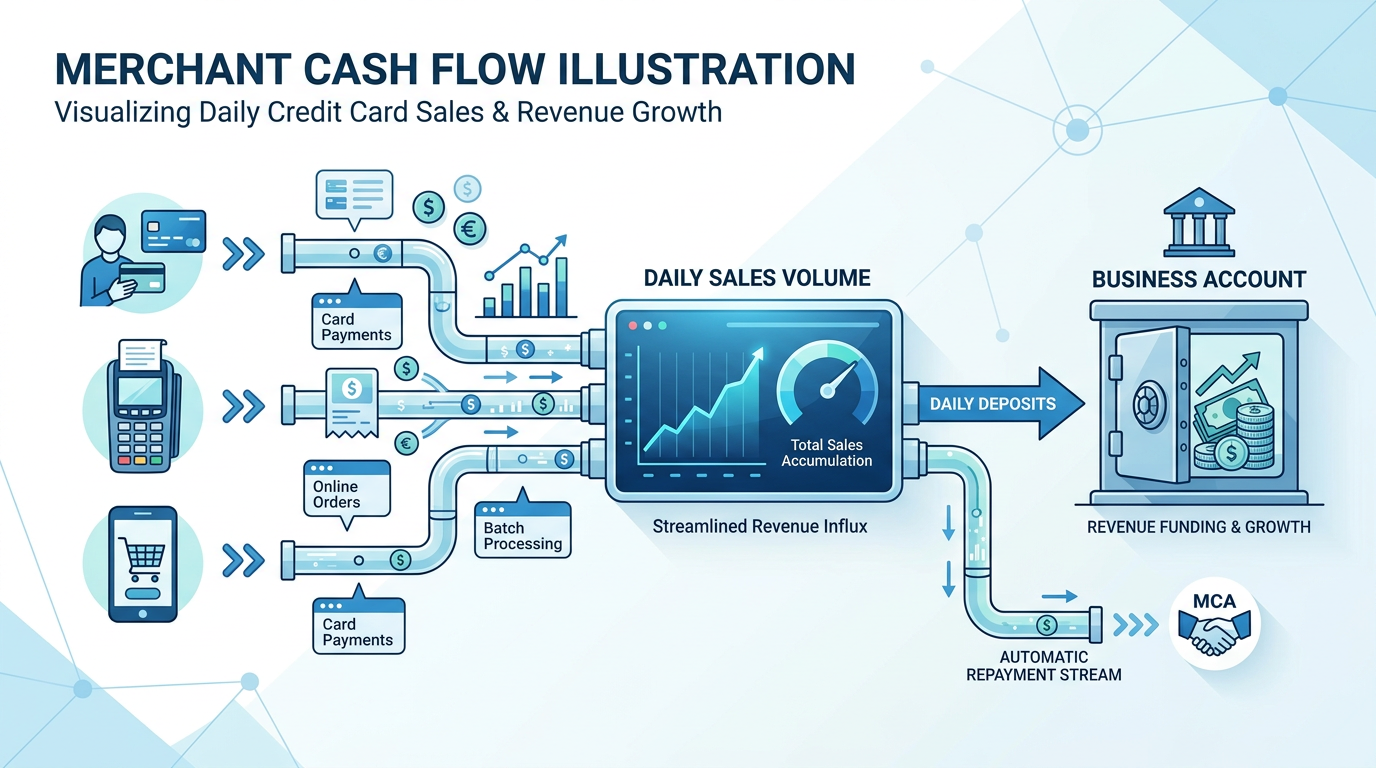

A merchant cash advance (MCA) is upfront capital repaid as a percentage of your daily credit card sales or through daily or weekly bank debits. You receive a lump sum and repay via a “holdback”—a fixed percentage of each day’s card sales or a fixed daily/weekly withdrawal from your business bank account. When sales are strong, you pay more and finish faster. When they dip, payments scale down. That flexibility suits businesses with variable daily traffic: restaurants, retail, salons, and others that accept card payments.

Unlike traditional term loans, MCA uses a factor rate (not APR) and repayment ties directly to revenue. Designed for businesses with consistent card volume, it offers one of the fastest paths to capital when you need it quickly. Axiant Partners connects U.S. businesses in all 50 states with merchant cash advance providers. We evaluate your card volume and deposits, compare offers, and match you with programs that fit. One application, multiple options. Apply now to see what you qualify for.

Many business owners confuse merchant cash advance with revenue-based financing or working capital loans. While all provide capital for operations, MCA is distinct: it focuses on daily card sales or bank deposits, typically funds faster than most alternatives, and uses a factor rate rather than an annual percentage rate. Understanding these differences helps you choose the right structure for your situation.

Businesses with strong card sales use merchant cash advances for short-term operational needs, seasonal gaps, and quick opportunities. From payroll during slow weeks to inventory buildup before the holidays, here’s how businesses put MCA funding to work:

Cover payroll during slow periods, when receivables lag, or when scaling staff. Restaurants, retail, and service businesses often face payroll due dates before revenue arrives. MCA provides fast access to keep your team paid and operations running without draining reserves.

Stock up before busy seasons, secure bulk discounts, or bridge ordering gaps. Retail and seasonal businesses rely on MCA to maximize sales windows. Holiday rushes, back-to-school, and summer peaks require inventory and staffing before sales materialize.

Unexpected expenses, a sudden opportunity, or a timing gap between payables and receivables. MCA funds in 1-3 days when traditional loans would take weeks. Use for time-sensitive needs only, and plan to refinance when possible.

Repayment scales with sales. Slow days mean lower holdback. No fixed monthly payment to stress over. Cash flow stays aligned with performance. Ideal for businesses with variable daily traffic or seasonal patterns.

Fund marketing, a pop-up, or a short-term growth push. When you need capital fast and have strong card volume, MCA can bridge the gap. Use for advertising campaigns, limited-time promotions, or expansion opportunities with quick payback.

Address urgent repairs, revenue dips, or unexpected costs. MCA provides fast access when traditional financing isn’t an option. Equipment breakdowns, emergency repairs, or sudden opportunities require immediate capital. Use strategically and plan to refinance when possible.

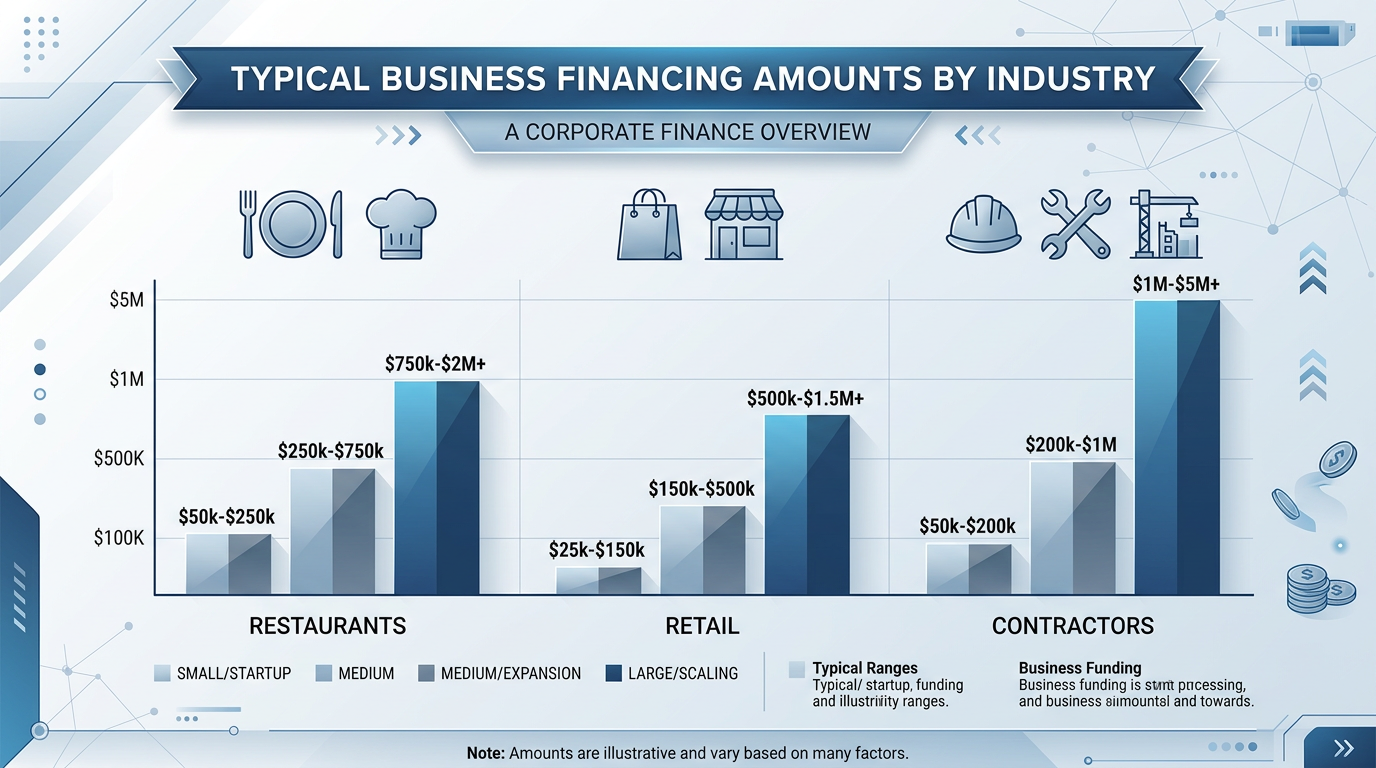

Merchant cash advances generally range from $5,000 to $500,000 depending on monthly card volume, bank deposits, and business profile. Funding size scales with how much you process in card sales or deposit regularly. Here are representative ranges we see across the U.S.:

Funding size scales with card volume and deposit consistency. Lenders review bank statements and merchant processing data. Use our calculator to estimate cash flow impact and repayment timing.

Merchant cash advances offer several advantages when speed and flexibility matter. Here’s why businesses with strong card volume choose MCA:

One of the fastest funding options available. Typical funding in 1-3 business days. Card volume and deposit verification drive underwriting—no lengthy SBA or bank timelines. When payroll is due or an opportunity can’t wait, MCA delivers.

Holdback flexes with daily performance. Strong sales days mean higher payments and faster payoff. Slow days mean lower holdback. No fixed monthly payment that strains cash flow during seasonal dips or unexpected slowdowns.

Use MCA for payroll, inventory, marketing, repairs, or any operational need. No restrictions on use. Deploy capital where it’s needed most to keep your business running and growing.

Borrow for operational needs instead of depleting savings. Keep reserves for emergencies and opportunities. MCA lets you bridge gaps without draining the bank account or missing payroll.

MCA uses a factor rate (e.g., 1.15 to 1.40) and a holdback percentage. You receive an advance and agree to repay the advance plus the factor by either:

Repayment flexes with sales when tied to card volume. Slower days mean lower payments. Understand total cost (factor rate, holdback, and timeframe) and cash flow impact before committing. We help you compare offers and choose wisely. Consider working capital loans or revenue-based financing if you prefer different repayment structures.

Providers offer different MCA structures based on business profile and needs. The right choice depends on card volume, deposit history, and how you prefer repayment:

Repayment as a percentage of daily card sales. Best for businesses with consistent in-person card volume. Holdback flexes with sales. Common in restaurants, retail, salons. Your merchant processor remits the holdback automatically.

Fixed daily or weekly ACH withdrawal from your business bank account. Best for businesses with strong deposits but variable card volume, or those that prefer predictable debits. E-commerce and B2B service companies often use this structure.

When time matters most. Fund up to $100,000 with same-day or next-day decisions. Streamlined applications, minimal documentation. Suited for urgent payroll, inventory, or time-sensitive opportunities.

For established businesses with consistent card volume. Advances up to $250,000. Decisions in 1-2 business days. Designed for restaurants, retail, and service businesses with 12+ months of history.

Deals above $250,000 for multi-location or high-volume operators. Review typically in 2-3 days. Built for significant operational needs, inventory buys, or expansion.

Some providers work with businesses under one year. Requirements may be stricter; amounts lower. Solid card volume and clean bank history improve odds. We connect you with options that fit your profile.

Programs exist for businesses rebuilding credit. Card volume and deposit history often matter more than FICO. Terms may reflect risk, but qualified borrowers can still access capital. Plan to refinance as your profile improves.

Understanding the differences helps you choose the right structure. RBF vs MCA—full comparison.

MCA: Repayment typically daily or weekly from card sales or bank debits. Often funds in 1-3 days. RBF: Repayment monthly as a percentage of revenue. May offer clearer terms. Both tie repayment to sales; RBF is often preferred for larger amounts and growth companies with stable monthly revenue. Compare RBF vs MCA.

MCA: Factor rate, flexible repayment tied to sales. Fast funding. Higher effective cost. Term loan: Fixed monthly payments, APR. Lower total cost for established businesses. MCA for urgent short-term needs; term loans for defined projects with predictable cash flow. Compare term loans.

MCA: Lump sum, fixed repayment schedule. Line of credit: Revolving access, draw and repay as needed. MCA for one-time needs; LOC for ongoing liquidity. Consider business line of credit if you need recurring access.

Requirements vary by provider, but many businesses qualify if they have:

Programs exist for both strong and challenged credit. MCA is designed for businesses with consistent sales. If you have lower card volume, consider working capital loans or revenue-based financing. Apply to see what you qualify for.

Axiant Partners connects you with merchant cash advance providers and guides you from application to funding.

Tell us about your business, card volume, and use of funds. One application goes to multiple MCA partners. We screen for fit and match you with providers that serve your profile.

Bank statements, merchant processing statements, and basic business info. Providers verify sales and deposits. We coordinate what’s needed and keep the process moving.

Advance amount, factor rate, holdback percentage. Compare offers if we match you with multiple providers. Select the structure that fits your cash flow and timeline.

Typical funding in 1-3 business days. Funds hit your account. Repayment begins per your agreement. Use capital where it’s needed.

MCA programs often fund in 1-3 days. Card volume and deposit verification drive the timeline.

Restaurants and food service businesses run on card sales. Payroll, inventory, and seasonal rushes create cash flow gaps. MCA ties repayment to daily sales—when traffic is strong, you pay down faster; when it’s slow, payments scale down. No fixed monthly payment during the post-holiday lull or unexpected slow weeks.

Typical amounts range from $20,000 for smaller operations to $150,000+ for multi-location restaurants. Funding in 1-3 days supports urgent needs: payroll before a busy weekend, inventory for a catering job, or emergency repairs. Restaurant financing · Apply now.

Retail and seasonal businesses face inventory buildup and staffing needs before peak sales. Holiday rushes, back-to-school, and summer spikes require capital before revenue arrives. MCA provides fast capital when you need it. Repayment ties to card sales—busy days mean higher payments, post-season lulls mean lower.

Typical amounts range from $25,000 for smaller retailers to $250,000+ for multi-location operations. Stock up, hire seasonal staff, and maximize sales windows. Apply now.

We work with businesses across many industries that process card sales or have consistent bank deposits, including:

Our goal is to provide financing solutions that support business growth—regardless of industry. If you have strong card volume or bank deposits, we can help match you with MCA providers that serve your sector.

Explore related financing: Working Capital Loans (fixed repayment) · Business Line of Credit (revolving) · Revenue-Based Financing (monthly revenue %) · All services

Merchant cash advances have tradeoffs. Understand them before you apply:

Proper use case selection matters. We help you determine if MCA fits your situation and walk you through total cost and cash flow impact before you commit.

We focus on connecting you with the right MCA provider and moving your application to funding.

One application, multiple options, support through funding. Apply now.

A merchant cash advance (MCA) is upfront capital repaid as a percentage of daily card sales or through daily/weekly bank debits. You receive a lump sum and repay via holdback until satisfied. Structurally, it’s a sale of future receivables, not a loan. Apply to learn more.

Typical funding in 1-3 business days. Card volume and deposit verification drive underwriting. One of the fastest funding options for businesses with strong card sales. Expedited programs often decide same-day or next-day.

Typically $5,000 to $500,000 based on monthly card volume, bank deposits, and business profile. Strong card sales and consistent deposits improve qualification. Multi-location or high-volume businesses often access higher amounts.

Both tie repayment to sales. MCA typically uses daily/weekly percentage of card sales or bank debits. RBF uses monthly revenue percentage. RBF may offer clearer terms; MCA often funds faster. Compare RBF vs MCA.

Card volume and deposit history often matter more than credit. Many programs work with 500+ FICO. Strong sales improve qualification. Apply to see your options. We match you with providers that fit your profile.

Yes. Once your business is stable, consider refinancing with a term loan or line of credit for lower cost. Our debt consolidation guide covers strategies.

Explore our MCA guides, RBF comparison, and working capital alternatives.

Structure, factor rates, holdback repayment, and when MCA fits your business.

Read moreSame-day decisions, 1-3 day funding, and what accelerates your advance.

Read moreAdvance limits, factor rates, and what drives your MCA amount.

Read moreCompare RBF and MCA—structure, repayment, cost, and which fits your business.

Read moreIf your business needs fast capital tied to card sales, our team can help. Submit an application today. We’ll match you with MCA providers and guide you through to funding.